House vs Flat UK 2025: An Expert’s Analytical Guide to Your Property Dilemma

The dream of homeownership remains a cornerstone of British ambition, yet the journey to securing that perfect abode in 2025 is rarely straightforward. With a dynamic property market, evolving financial landscapes, and shifting lifestyle priorities, many aspiring homeowners find themselves at a crucial crossroads: should I buy a house or a flat? This isn’t merely a question of bricks and mortar; it’s a profound interrogation of finances, freedom, future aspirations, and the very fabric of your daily life.

As an expert who has navigated the intricacies of the UK property market for over a decade, I understand the weight of this decision. The choice between a house and a flat in 2025 is more nuanced than ever, influenced by factors ranging from the latest mortgage rates UK 2025 to the ongoing discourse surrounding leasehold reform UK. This analytical guide will delve deep into the pros and cons of each option, offering a comprehensive perspective to help you make an informed and confident decision.

The Evolving UK Property Landscape in 2025: A Snapshot

Before we dissect the house vs. flat debate, it’s essential to set the stage with the prevailing market conditions. In 2025, we’re observing a property market characterised by several key trends:

Moderated Price Growth: While the frenzied pace of post-pandemic appreciation has largely settled, regional variations in UK property investment remain significant. Demand in desirable urban centres and commuter belts continues to outstrip supply, particularly for family homes.

Interest Rate Volatility: Though potentially stabilising, the era of ultra-low interest rates is firmly behind us. This impacts mortgage affordability across the board, making careful budgeting and financial planning paramount, especially for first-time buyer UK schemes.

Cost of Living Pressures: Broader economic challenges continue to influence disposable income, prompting buyers to scrutinise every aspect of property ownership, from initial purchase costs to ongoing property maintenance costs UK and utility bills.

Sustainability as a Priority: Energy efficiency is no longer a niche concern. With rising energy costs and a collective drive towards net-zero, properties with high energy efficiency ratings property are increasingly sought after, impacting both value and running expenses.

Flexible Working Models: The hybrid work model is firmly embedded, influencing demand for properties that offer dedicated home office spaces or are located in areas with a better work-life balance, sometimes favouring suburban houses over central flats, but also boosting the appeal of well-designed urban flats.

Understanding this backdrop is crucial, as it shapes the inherent advantages and disadvantages of both houses and flats in today’s market.

The Enduring Appeal of a House: Space, Freedom, and a Piece of Land

For many, the quintessential British dream involves a house, complete with a garden and a sense of absolute ownership. In 2025, the appeal remains strong, particularly for growing families or those seeking a sanctuary away from the urban hustle.

Advantages of House Ownership in 2025:

Unparalleled Space and Flexibility: This is arguably the most significant draw. A house typically offers more internal square footage, allowing for multiple bedrooms, dedicated living areas, and often a garden. The ability to extend, convert a loft, or build a conservatory provides invaluable flexibility as your family grows or your lifestyle changes. Think of the potential for a home gym, a dedicated office, or a playroom – possibilities that are often constrained in a flat. The garden, whether a modest patio or a sprawling lawn, offers private outdoor space for relaxation, entertaining, or simply a safe play area for children and pets. This becomes a significant factor in promoting well-being and a stronger connection to nature.

Privacy and Independence: Living in a house generally means fewer shared walls, floors, or ceilings with neighbours, leading to greater acoustic privacy and a reduced likelihood of noise disputes. You have greater autonomy over your property, from exterior aesthetics to internal alterations, without needing permission from a management company or freeholder. This sense of self-determination and control over your immediate environment is a powerful psychological benefit.

Long-Term Investment & Freehold Value: Historically, houses tend to appreciate more consistently than flats, largely due to the land component. When you buy a house, you typically acquire the freehold property advantages, meaning you own both the building and the land it sits on outright. This eliminates concerns about diminishing lease lengths, escalating ground rent charges (a common flat issue, even with reforms), or unpredictable service charges. Land value is a stable asset, offering a strong foundation for long-term wealth building and making a house a robust form of UK property investment. Should you decide to sell in the future, the freehold title is often simpler and more attractive to buyers.

Customisation and Personalisation: Your house is your canvas. Without the stringent rules often imposed by leasehold agreements, you have considerable freedom to renovate, redecorate, and adapt your home to your precise tastes and needs. This ability to infuse your personality into your living space is a major draw, allowing you to create a truly bespoke environment. From a new kitchen to a full extension, you control the improvements, which in turn can significantly increase your property’s value.

Community and Lifestyle: While often associated with suburban or rural settings, houses foster a different kind of community spirit. Neighbourhoods with streets of houses often have local parks, schools, and community events that encourage interaction among residents. For families, the proximity to good schools and green spaces is often a deciding factor, contributing to a desirable suburban house prices UK premium.

Disadvantages of House Ownership in 2025:

Higher Initial Investment and Costs: Houses typically command a significantly higher purchase price than flats, especially in desirable areas. This translates to a larger deposit, higher stamp duty UK outlays, and potentially larger mortgage rates UK 2025 repayments. For first-time buyer UK schemes, this can often make houses financially out of reach without substantial savings or family assistance.

Extensive Maintenance and Upkeep: The buck stops with you. As a homeowner, you are solely responsible for all repairs, maintenance, and upkeep, both internal and external. This includes everything from roof repairs, boiler servicing, and garden maintenance to dealing with pests or structural issues. These tasks can be time-consuming, physically demanding, and, crucially, expensive, adding considerably to your property maintenance costs UK. Unexpected expenses can quickly erode savings, making a substantial emergency fund essential.

Increased Running Costs: Larger properties naturally consume more resources. Heating and cooling a house, particularly older builds, can be significantly more expensive than a smaller flat, impacting your cost of living UK property. Council tax bands UK are also generally higher for houses compared to flats in the same area. Furthermore, house insurance premiums can be higher due to the larger size and potentially greater risk factors.

Potential for Isolation and Inconvenience (Location Dependent): While suburban and rural houses offer peace, they often mean being further away from immediate amenities, transport links, and city centres. This can necessitate greater reliance on a car and longer commutes, which impacts both time and money. For those who thrive on immediate access to shops, restaurants, and cultural venues, a house outside a vibrant urban hub might feel isolating.

Environmental Footprint: Older, larger houses can sometimes have a less favourable environmental profile. While renovations can improve energy efficiency ratings property, many older homes require significant investment to meet modern standards. Larger surface areas and volumes generally mean greater energy consumption, contributing to a higher carbon footprint and larger utility bills if not addressed.

The Modern Allure of a Flat: Convenience, Community, and a Gateway to Urban Life

Flats, once seen by some as a compromise, have increasingly become the preferred choice for a diverse range of buyers in 2025 – from young professionals and first-time buyer UK schemes to downsizers and investors. They represent a pragmatic and often more accessible route into the property market, particularly in urban areas.

Advantages of Flat Ownership in 2025:

Enhanced Affordability and Accessibility: Flats typically have lower purchase prices compared to houses, making them a more accessible entry point for many, especially those looking to buy in competitive urban markets. This often means lower deposits, reduced stamp duty UK, and more manageable mortgage affordability. Schemes like shared ownership UK are also predominantly available for flats, further widening access to homeownership. For those with a more limited budget, a flat can be the crucial first step on the property ladder.

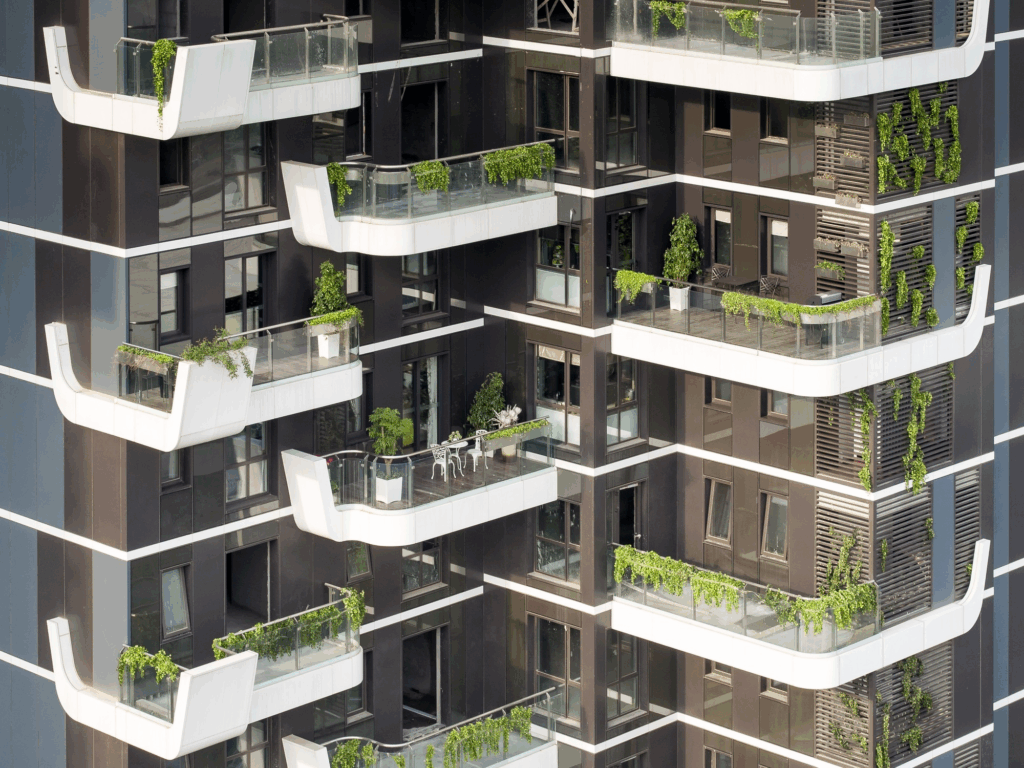

Prime Locations and Urban Convenience: Flats are frequently found in desirable city centres, bustling towns, and well-connected transport hubs. This offers unparalleled convenience, with shops, restaurants, entertainment venues, and public transport options often within walking distance. This city living advantages UK extends to quicker commutes, access to cultural events, and a vibrant social life, appealing strongly to those who value immediate access to amenities and a dynamic urban environment. Many modern developments also boast excellent sustainable living UK credentials due to their proximity to services, reducing reliance on private vehicles.

Lower Maintenance and Shared Responsibilities: A major draw of flat ownership is the reduced personal responsibility for external maintenance. Building management (funded by your service charges flat UK) typically handles communal areas, structural repairs, roofing, and external upkeep. This frees up your time and often means predictable costs for major works, rather than unexpected large bills. This “lock up and leave” lifestyle is highly attractive to busy professionals, frequent travellers, or those downsizing property UK who want to minimise chores.

Modern Amenities and Security: Many new-build flats come equipped with desirable amenities such as gyms, swimming pools, concierge services, communal gardens, and secure parking. These facilities significantly enhance quality of life and often come at a lower individual cost than if you were to pay for them privately. Furthermore, flats often benefit from robust security systems, including CCTV, entryphones, and secure entrances, offering an added layer of peace of mind.

Energy Efficiency and Sustainability: Modern flats are generally built to higher energy efficiency ratings property standards than older houses, with superior insulation, double glazing, and efficient heating systems. Their smaller surface areas and shared walls contribute to less heat loss, resulting in lower utility bills and a reduced carbon footprint, aligning with growing concerns for sustainable living UK.

Community Living: While different from a street of houses, flats often foster a strong sense of community, particularly in managed blocks with shared facilities. Neighbours are in closer proximity, often leading to more social interaction and a ready network of support.

Disadvantages of Flat Ownership in 2025:

Less Space and Limited Freedom: Flats inherently offer less internal space and often lack private outdoor areas (though balconies or communal gardens can compensate). Storage can be a significant challenge. Furthermore, the ability to personalise your space is often restricted by leasehold covenants. Major alterations, such as knocking down a wall, typically require permission from the freeholder, which can be a lengthy and costly process, or even prohibited entirely.

Leasehold Complexities and Costs: The vast majority of flats in the UK are sold on a leasehold basis. While leasehold reform UK is ongoing, leasehold can still involve complex legalities and additional costs. Key concerns include:

Ground Rent Charges: An annual fee paid to the freeholder, which can escalate over time. While reforms aim to abolish or cap these, existing leases may still be affected.

Service Charges Flat UK: Annual payments for the maintenance, repair, and insurance of communal areas and the building’s structure. These can be substantial and unpredictable, especially for major works.

Lease Extensions: As the lease term diminishes (especially below 80 years), extending it becomes increasingly expensive and vital for resale value, adding a significant future cost.

Freeholder Disputes: Conflicts can arise over service charge reasonableness, building management, or permission for alterations. This lack of full autonomy can be a source of frustration.

Less Privacy and Potential for Noise: Sharing walls, floors, and ceilings inevitably means less privacy. Noise from neighbours, whether it’s footsteps, music, or conversations, can be a common source of irritation and disputes, particularly in older buildings with poorer sound insulation. Your lifestyle choices might also be constrained by noise considerations for your neighbours.

Slower Capital Appreciation: While regional variations exist, flats have historically shown slower capital appreciation compared to houses, primarily because they do not include land value and are subject to leasehold depreciation. This can make them a less potent UK property investment for long-term wealth growth, though their accessibility makes them an excellent stepping stone.

Restrictions on Pets and Lifestyle: Many leasehold agreements have covenants restricting pet ownership, sub-letting, or even certain types of activities, limiting your lifestyle choices. This can be a significant drawback for animal lovers or those planning to use the property for investment purposes like buy-to-let UK.

Key Factors for Your 2025 Property Decision

Navigating the choice between a house and a flat requires a rigorous self-assessment against several critical factors in the current market climate:

Budget and Financial Goals:

Affordability: Realistically assess your total budget, including deposit, mortgage rates UK 2025, stamp duty UK, legal fees, and moving costs. Remember that a higher purchase price for a house means higher initial outlays.

Long-Term Investment Strategy: Are you looking for maximum capital appreciation or a secure entry point into the market? Houses typically offer greater long-term growth potential due to land value, while flats can be a solid, more affordable initial UK property investment. Consider the impact of lifetime ISA property bonuses if you’re a first-time buyer, as this fund can be applied to either.

Ongoing Costs: Factor in council tax bands UK, utility bills, insurance, and whether you’re prepared for fluctuating property maintenance costs UK (house) or predictable but potentially high service charges flat UK and ground rent charges (flat).

Lifestyle and Family Needs:

Space Requirements: Do you need multiple bedrooms, a garden for children or pets, or dedicated work-from-home spaces? Houses offer more inherent flexibility for growing families.

Privacy vs. Community: How important is absolute privacy to you? Are you comfortable with shared living spaces and potentially closer proximity to neighbours?

Time Commitment: Are you prepared for the significant time investment required for house maintenance and gardening, or do you prefer a “lock up and leave” lifestyle?

Pets: If you have pets or plan to get them, check leasehold restrictions for flats carefully.

Location and Transport Needs:

Urban vs. Suburban vs. Rural: Flats dominate city centres, offering unparalleled city living advantages UK. Houses are more prevalent in suburban and rural areas. Consider your commute, access to amenities, and desired lifestyle.

Transport Links: Evaluate public transport accessibility. Flats are often strategically located near train stations and bus routes, while houses may require a car, impacting your cost of living UK property.

Investment Horizon and Future Plans:

Short-Term vs. Long-Term: How long do you plan to stay in the property? A short-term move might favour the affordability and ease of a flat, while a long-term plan might lean towards the greater appreciation potential of a house.

Future Growth: Do you anticipate needing more space in the future for a growing family? Will your work situation change? Consider how adaptable each property type is to your evolving needs, including potential for downsizing property UK later in life.

Maintenance Tolerance:

Are you a keen DIY enthusiast, or would you prefer to outsource most maintenance tasks? Houses demand a more hands-on approach, whereas flat ownership delegates much of the external upkeep.

Regulatory Landscape (2025 Specific):

Leasehold Reform UK: Stay updated on the latest developments. While reforms aim to improve leaseholder rights, existing issues could still impact the appeal and costs associated with flats.

Energy Performance Certificates (EPCs): With increasing emphasis on green homes, the energy efficiency ratings property will become even more critical for both houses and flats, affecting resale value and financing.

Making an Informed Choice in 2025

There is no universally “correct” answer to the house vs. flat dilemma. The optimal choice is deeply personal, reflecting your unique financial standing, lifestyle aspirations, and future goals in the context of the 2025 property market.

Begin by performing a thorough financial audit. Understand exactly what you can afford, not just for the purchase, but for the ongoing costs and potential future expenses. Utilise online tools for initial property valuation UK estimates, but always seek professional advice for a more accurate assessment.

Next, conduct a lifestyle audit. Envision your ideal daily life five or ten years from now. Where do you want to be? What kind of space do you need? How much time and energy are you willing to dedicate to your home?

Finally, don’t underestimate the value of professional guidance. Engaging with local estate agents who have an intimate understanding of specific areas can provide invaluable insights into market trends, typical property types, and hidden costs for both houses and flats. They can help you sift through the complexities, understand the nuances of freehold property advantages versus leasehold structures, and navigate the current mortgage rates UK 2025 environment.

The decision to buy a house or a flat in 2025 is a significant milestone. By analytically weighing the advantages and disadvantages, aligning them with your personal circumstances, and leveraging expert advice, you can embark on your homeownership journey with clarity and confidence, securing a home that truly fits your life.