Navigating the UK Buy-to-Let Landscape: Houses vs. Flats in 2025

The UK property market, a perennial topic of national fascination and fervent discussion, enters 2025 still buzzing with activity, albeit with its unique set of complexities and opportunities. As an investor who’s navigated these waters for over a decade, I’ve witnessed cycles of boom and bust, regulatory shifts, and evolving tenant demands. Today, the landscape is defined by persistent housing shortages, robust rental demand, and a growing emphasis on sustainability, all set against a backdrop of stabilising, yet still significant, interest rates.

For prospective and seasoned buy-to-let investors alike, a foundational decision often looms large: should your capital be deployed into a standalone house or a unit within a larger block, commonly known as a flat? Both offer distinct pathways to generating wealth through rental income and capital appreciation, but their respective charms and challenges cater to different investment appetites and strategic goals. This isn’t merely a preference; it’s a strategic choice that will profoundly impact your cash flow, management responsibilities, and long-term portfolio growth.

In this comprehensive guide, we’ll peel back the layers of these two primary residential asset classes, offering insights from a decade in the trenches and framing them within the prevailing 2025 market conditions. Our aim is to equip you with the clarity needed to make an informed decision that aligns with your financial aspirations and risk tolerance within the dynamic UK property investment sphere.

Understanding the Fundamental Distinctions in the UK Context

Before delving into the intricate comparisons, let’s establish a clear understanding of what we mean by “house” and “flat” in the context of UK buy-to-let investment.

Houses: In the UK, a house typically refers to a standalone residential dwelling, or one with direct access to the street and often a private garden, regardless of whether it’s detached, semi-detached, or terraced. Ownership is usually freehold, meaning you own both the building and the land it sits on outright. These properties are often acquired with a standard residential mortgage or, for investors, a buy-to-let mortgage UK. As of recent data, houses make up the vast majority of the UK’s 29 million dwellings, representing a traditional and often sought-after form of accommodation.

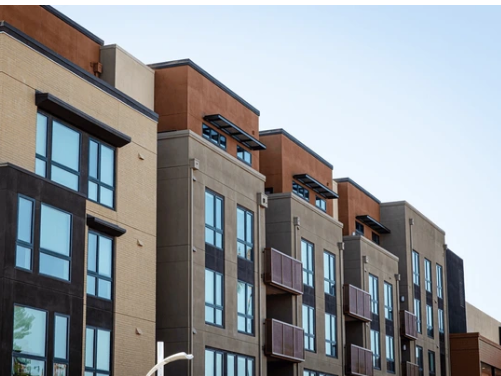

Flats: A flat, or apartment, is a self-contained residential unit within a larger building, sharing common structural elements like walls, floors, and roofs with other units. Ownership is typically leasehold, meaning you own the right to occupy the property for a fixed period (the lease) but not the land or the building’s structure itself. The freehold is usually owned by a separate entity (the freeholder) or collectively by the leaseholders. Flats are particularly prevalent in urban centres and purpose-built blocks, with millions across the UK offering convenient apartment living arrangements. Investment in flats often involves navigating service charges, ground rent, and the intricacies of block management.

The Decisive Factors: Houses vs. Flats for Your 2025 Portfolio

Your journey to a successful UK property portfolio hinges on evaluating several critical aspects. Here, we dissect ten key considerations through the lens of a seasoned UK property expert.

Investment Objectives & Financial Returns

Understanding your core objective is paramount. Are you chasing immediate rental yield UK or long-term capital appreciation UK property?

Cash Flow (Rental Yield): Flats, particularly those in high-demand urban areas or near universities (ideal for student accommodation investment UK), can offer attractive rental yields due as they often appeal to a broader tenant demographic – young professionals, students, or single occupants – who value location over expansive space. Multi-unit investments like Houses in Multiple Occupation (HMOs), which are often houses converted into multiple rentable rooms, can generate significantly higher cash flow, albeit with increased regulatory burdens and management intensity. For a standard house, a single vacancy means zero income, whereas a flat in a multi-unit block still provides income from other units, offering a degree of stability.

Capital Appreciation: Historically, houses, particularly those with freehold ownership and private outdoor space, have often seen stronger capital appreciation. The scarcity of land and the enduring aspiration for a family home often drive this trend. While flats in prime locations can also see substantial growth, their appreciation can sometimes be limited by the perceived value of the building as a whole and the remaining lease term. However, value-add strategies – such as refurbishing outdated flats – can significantly boost their market value.

Risk Diversification: Investing in multiple flats within different blocks, or even a portfolio of HMOs, offers inherent risk diversification. A void period in one flat has a lesser impact on your overall income than a vacant single-family home. This strategy provides a buffer against market fluctuations or individual tenant issues, making it a cornerstone of prudent passive income property UK strategies.

Ownership Structure & Management Complexity

The nature of ownership profoundly impacts your responsibilities and operational involvement.

Houses: Owning a house usually means outright freehold, granting you full control over the property. You are solely responsible for all maintenance, repairs, insurance, and compliance. This direct control can be appealing for hands-on investors. Tenants typically deal directly with you, the private landlord, allowing for a more personalised relationship, though this also means you are the first point of call for all issues.

Flats: The leasehold structure of flats introduces additional layers of ownership. You own the lease, but a freeholder or a management company (often appointed by the freeholder) is responsible for the building’s communal areas, structure, and major systems. This necessitates paying service charges and ground rent, which can be substantial. While this offloads some maintenance burden, it also means less direct control over decisions regarding the building’s exterior or communal spaces. Renters usually interact with a property management company, which can streamline operations but also add another layer of communication.

Physical Structure & Development Potential

The physical attributes dictate much about appeal and potential modifications.

Houses: Offer standalone living, often with potential for extensions (subject to planning permission) or internal reconfigurations. Terraced, semi-detached, or detached houses provide a distinct sense of privacy and space. Their structure allows for more individual customisation and potential future expansion, which can add significant value.

Flats: Are units within a larger structure, sharing walls, floors, and ceilings. While internal alterations are usually possible (with freeholder consent), exterior changes or structural extensions are generally not. Modern Build-to-Rent (BTR) developments often feature impressive communal facilities such as gyms, co-working spaces, and resident lounges, which enhance their appeal, particularly to younger demographics seeking a vibrant community lifestyle.

Space, Layout & Target Tenant Demographics

The size and configuration of your investment will largely determine its attractiveness to different segments of the UK rental market.

Houses: Typically offer greater square footage and more rooms, making them highly desirable for families, couples seeking more space, or those working from home. Properties with gardens are especially sought after. The average size of a house in the UK varies widely by region but generally exceeds that of a flat, catering to tenants who value space and outdoor living.

Flats: Are generally more compact. One, two, and three-bedroom flats are common, appealing to single professionals, young couples, or students. Their smaller footprint means lower utility bills and less cleaning, which can be attractive. The average flat size can range significantly, but they are consistently smaller than houses, reflecting their urban-centric appeal.

Maintenance & Regulatory Compliance

Both property types demand ongoing maintenance, but the scope and responsibility differ significantly. Landlords must also contend with the evolving regulatory landscape, especially regarding Energy Performance Certificate (EPC) UK landlord requirements.

Houses: As the sole owner, you are responsible for all aspects of maintenance:

Exterior: Roof, gutters, walls, windows, doors, and foundations.

Interior: Plumbing, electrical systems, heating, appliances, and general wear and tear.

Grounds: Gardens, driveways, fences.

Key Systems: Boiler servicing, electrical safety checks (EICR), gas safety certificates (CP12).

EPC: Meeting increasingly stringent energy efficiency standards can mean substantial upgrade costs for older properties, a key consideration for UK property market forecast 2025.

Flats: While internal maintenance is your responsibility, the building’s exterior, roof, communal areas, and major systems (e.g., lift, communal heating) are managed by the freeholder or management company, funded by your service charges.

Common Areas: Hallways, lobbies, stairwells, lifts, gyms, and communal gardens.

Building Systems: Central heating, fire alarms, intercoms, and security features.

Safety & Compliance: Regular fire risk assessments and other statutory inspections of the entire building.

Leasehold Covenants: Adhering to the terms of your lease, which can restrict certain alterations or uses.

Amenities & Lifestyle Appeal

The amenities offered can significantly influence tenant demand and rental value.

Houses: Often come with private amenities such as gardens, off-street parking, garages, and the potential for custom interior upgrades like bespoke kitchens or bathrooms. These features appeal to tenants seeking privacy and personal space.

Flats: Especially in modern developments, can boast an impressive array of shared facilities: fitness centres, swimming pools, concierge services, communal lounges, and secure bike storage. These conveniences are a major draw for tenants, particularly in urban areas, who value lifestyle benefits and community. However, maintaining these shared facilities adds to the service charge burden.

Privacy & Community Dynamics

The living environment impacts tenant satisfaction and potential issues.

Houses: Provide unparalleled privacy. With space between properties, private gardens, and no shared internal walls (for detached homes), tenants enjoy a greater sense of seclusion. This often appeals to families and those seeking a quieter lifestyle.

Flats: Involve shared living environments, with closer proximity to neighbours. Noise transmission between units can be a factor. Common areas like hallways, lifts, and shared gardens mean more frequent interactions. While some tenants appreciate the sense of community, others may find the lack of absolute privacy challenging.

Cost Structure & Financial Outlay

Beyond the initial purchase price, the ongoing costs vary considerably. Navigating Stamp Duty Land Tax (SDLT) buy-to-let and mortgage interest relief changes are crucial.

Houses: Landlords bear all direct property costs: buy-to-let mortgage UK repayments, council tax, landlord insurance, maintenance, and utility bills during vacant periods. SDLT on additional properties is a significant upfront cost. While there are no service charges or ground rent, the lack of shared costs means all expenses for repairs fall solely on you.

Flats: A more complex cost structure. In addition to mortgage, council tax, and insurance, you’ll pay service charges (for building maintenance, communal areas, amenities) and ground rent to the freeholder. While these charges add to the monthly outlay, the economies of scale in managing a larger block can sometimes lead to lower per-unit costs for certain large-scale repairs compared to managing a detached house.

Scalability & Portfolio Expansion Strategies

Consider how easily you can grow your property investment strategies UK portfolio.

Flats: Scaling a portfolio of flats, especially within a single block or development, can offer centralized management benefits. Acquiring multiple units from one developer or in a concentrated area simplifies logistics. However, each acquisition still represents a substantial capital investment. For those building a large portfolio, this can be a more efficient path to growth.

Houses: Expanding a portfolio of single-family homes often requires finding properties in diverse locations, which can be more “people-intensive” in terms of management and maintenance across different neighbourhoods. The BRRRR (Buy, Refurbish, Refinance, Rent, Repeat) strategy, while popular in some markets, requires careful execution in the UK given lending criteria and market fluidity. Each house acquisition might require less initial capital than a block of flats, but the cumulative effort can be higher.

Market Dynamics & Future-Proofing for 2025

The UK market is constantly evolving, with new trends and regulations emerging.

Houses: Demand for family homes remains consistently strong, driven by demographics and lifestyle aspirations. However, older houses may face significant costs to meet impending EPC regulations. Location, school catchments, and transport links are paramount.

Flats: Benefit from strong demand in urban centres, driven by employment, education, and lifestyle. The rise of Build-to-Rent (BTR) schemes highlights institutional investor confidence in the flat rental market. Future-proofing involves selecting properties in areas with strong infrastructure investment and high tenant demand, and ensuring the building’s management is proactive in sustainability.

Making Your Move in the 2025 UK Buy-to-Let Arena

The choice between a house and a flat for your high-yield property UK investment is rarely straightforward. It’s a nuanced decision that demands careful consideration of your financial capacity, risk appetite, time commitment, and long-term vision.

As we navigate 2025, the UK property market continues to present robust rental property UK opportunities. Whether you lean towards the direct control and potential capital appreciation of a house, or the potential for higher yields and diversified risk of flats, success hinges on meticulous due diligence, a thorough understanding of the local market, and a keen eye on evolving regulations.

Don’t let the complexity deter you. Instead, view it as an invitation to refine your strategy and make truly informed decisions. The landscape is rich with potential for those willing to do the groundwork.

Are you ready to unlock your potential in the UK buy-to-let market? Explore properties tailored to your investment goals or connect with experienced professionals today to secure your financial future.